On the three-legged stool of taxation – sales, income, and property taxes – Utah is less regressive than most other states. This is important because some Utahns believe that higher-income earners should pay a larger percentage of their income. In contrast, others believe that higher-income earners should pay less since they already contribute the lion’s share of the overall state and local tax receipts.

Tax policy is perhaps one of the most widely and hotly debated national, state, and local issues. Many private organizations at each level venture into this well-known policy labyrinth, such as the Tax Foundation and the Utah Taxpayers Association. The Utah Foundation also routinely explores this topic, most recently with Balancing the Burden: Utahns’ Tax Burden is Up from Historical Low.

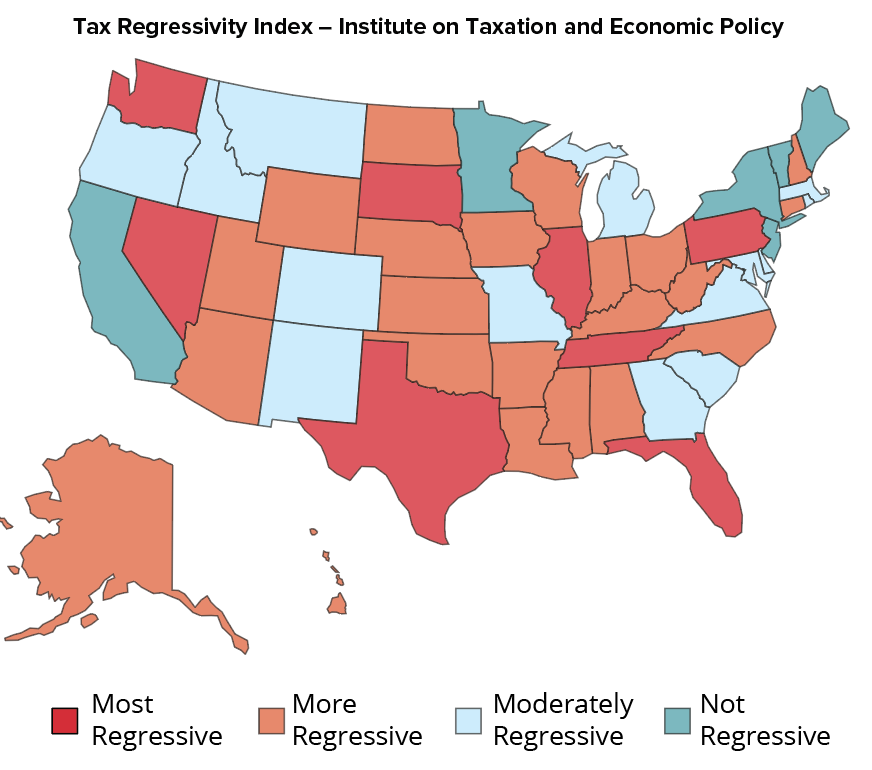

The Institute on Taxation and Economic Policy, a non-profit think tank, also recently released its newest tool, Who Pays? State-by-State Data, which investigates the topic. The data outline taxpayers’ burden by income level to understand precisely how regressive or progressive they are.

From a definitional perspective, if lower-income taxpayers spend a higher percentage of their income on taxes, then the state’s tax system is regressive. Conversely, if higher-income taxpayers do, then the system is deemed progressive or non-regressive.

Among the states with the most regressive tax policies, Florida is number one, followed by Washington, Tennessee, and Pennsylvania. On the opposite side of the discussion, Minnesota, Vermont, and New York exhibit non-regressive tax policies.

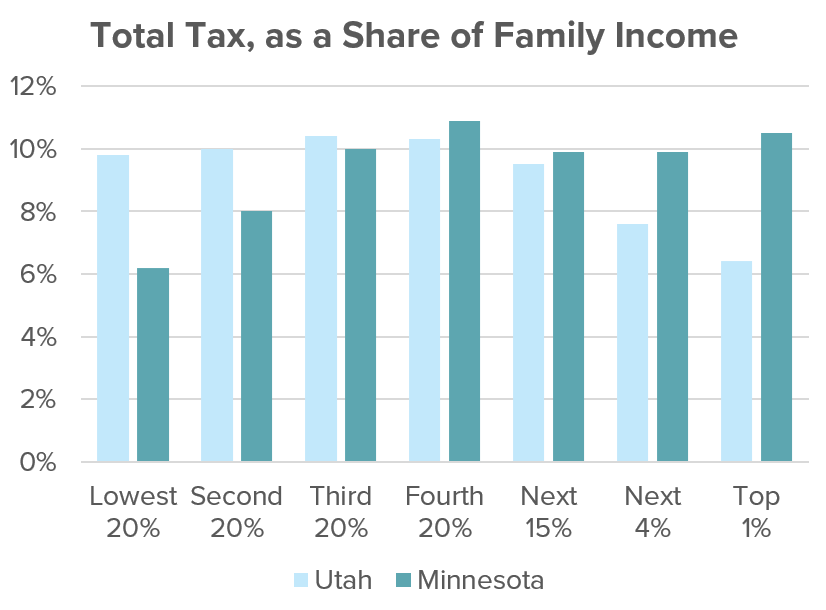

Utah ranks number twenty-nine for the most regressive state and local tax system in the country. When breaking down the data by tax type, the top 1% of Utah’s income bracket pays 3.8% of their income to personal income tax, while the lowest 20% pays 0.7%. This could be considered a non-regressive tax. However, the sales and excise taxes significantly impact Utah’s lower-income households as the lowest 20% pay 6.3% while the top 1% pay only 0.9% of their income in sales taxes, which could be considered regressive.

Minnesota, ranked as the least regressive state, shares similarities with Utah in its sales and excise tax statistics. The top 1% of Minnesota taxpayers also pay 0.9% of their income to sales and excise taxes (like Utah residents), with the lowest 20% paying 6% of their income. The two states differ in that the top 5% of Minnesota income earners pay notably more personal income tax than do Utahns. Furthermore, Minnesota’s lowest 20% income earners tie for the least in property taxes, while Utah’s lowest 20% pays the most. This shows that while any one tax can be pretty regressive or progressive, it is important to consider how they all work together as a total tax package.

Tax policy, in general, and the degree of regressive or progressive taxation might be considered a highly partisan issue. It, therefore, seems ironic that Utah – a solidly Republican state – is close to the “moderately regressive“ portion of the scale while Washington – a solidly Democratic one – is the second-most regressive. Perhaps it is appropriate to reconsider our understanding of various states’ political predilections or reconsider the degree to which tax policy truly reflects voter preferences in Utah and elsewhere.

Source: Institute on Taxation and Economic Policy, https://itep.org/whopays-map-7th-edition/.

Author: Research Intern Micaela McElrath and Utah Foundation staff.

Categories: