Does Student Debt Slow Utah Millennials Down?

The ballooning amount of student debt is startling. Across the country, it adds up to almost 1.3 trillion dollars in total. As a comparison, that is almost how much US currency is in circulation today. Moreover, the majority of that debt is carried by a demographic (22-26 year olds) that needs its borrowing power. A lot of research has shown that a high level of student debt slows major life events, such as marriage, having children, purchasing a first car or home, starting a business, or preparing for retirement savings.

{kind=link}

Lucky for Utah, student debt isn’t such a burden here. Although the average level of student debt has risen rapidly in the past seven years (74% increase), the average level of student debt in Utah ($22,418) is still the forty-fourth lowest in the nation. Even still, that’s an extra $230 per month of disposable income recent graduates have to pay in student loan payments for the next ten years. At the same time, the extra $833 dollars they earn per month from having earned a college degree likely eases that pain.

But is there evidence that Utahns are also delaying these life milestones due to student debt? To answer these questions we turn to our recent survey data.

Marriage and Kids

Initially, there appeared to be a link between student debt and marriage. However, after accounting for demographic factors such as age, education level, level of income, and religion, the link disappeared. As a result, it is possible that student debt might delay marriage in Utah, but there are a number of other factors that have a lot more influence over the decision.

Similar to marriage, there initially appeared to be a link between student debt and both the number of children and the presence of any children in families. However, once age, marital status, income, and religion were accounted for, there appeared to be no difference of the number or presence of children between those who had student debt and those who did not.

Housing Situation

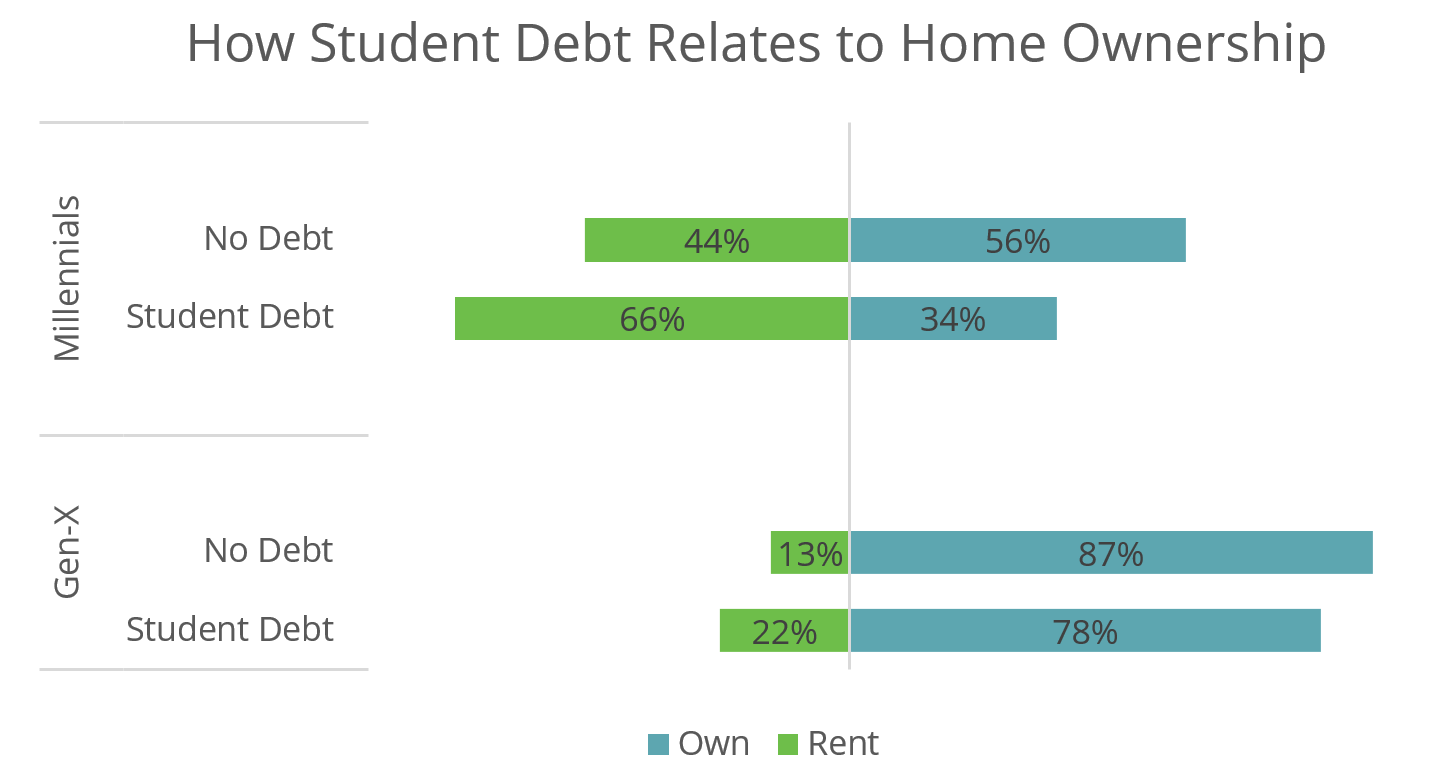

While some attribute the trend of Millennials living at home to a higher level of student debt, our survey results showed that living at home is linked more strongly to marital status and level of income rather than the presence or level of student debt.

However, our survey data does show that those who have student debt are 6% more likely to rent rather than own their own home, even after accounting for other variables. The impediment of student debt more than doubled when looking at just Utah Millennials. They were 14% less likely to own their own home. To be clear, we can’t conclusively prove that student debt causes people to delay home purchases. It might be that those who buy homes don’t continue their education and take out additional loans. Or there could be another factor that influences both. However, looking at the logical options and considering timing (education usually precedes home purchase), it does seem likely that student debt is slowing the rate of home purchases in Utah. That, however, doesn’t keep Utah from being the #2 state in the nation for homeownership among millennials.

Overall, it appears that student debt has a more limited effect on life milestones in Utah than nationally, probably a function of lower level of student debt among Utahns. And while it does impose a burden on an individual’s disposable income, the benefits of college education continue to outweigh the cost of leveraging credit to obtain it.

Categories: