In 2016, Utah Foundation’s Priorities Project found that citizens were more concerned about health care costs than any other issue. The lively debate over health care costs during the past decade has focused primarily on the implications of national policy. However, states have unique health care landscapes, needs and opportunities.

In Part 2 of the Utah Health Cost Series, Utah Foundation examines the employer-sponsored insurance market and the market for individuals purchasing insurance. Paying a Premium also analyzes national trends regarding health care affordability for Medicare recipients. Finally, the report examines the factors driving health insurance costs.

In a previous report, Utah Foundation looked at medical service costs. In a subsequent report, Utah Foundation will examine the costs associated with Medicaid spending in Utah.

Download the report, here.

Key Findings of this Report

- About 61% of Utahns purchase health insurance through employers. This is the highest in the nation and significantly higher than the U.S. average of 49%.

- Enrollment in high-deductible plans in Utah has increased from 3% to 30% during the past decade.

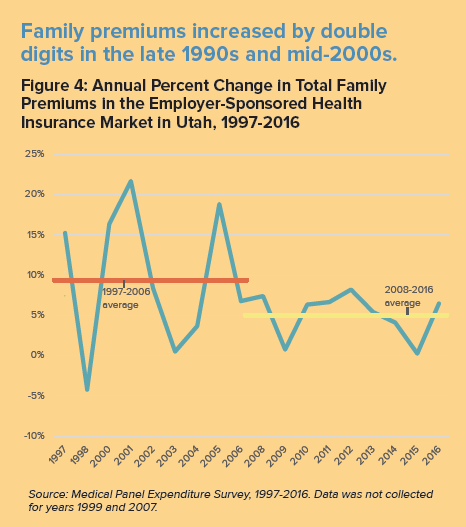

- The average total premium for an employer-sponsored individual plan in Utah increased by an inflation adjusted 34% from 2006 to 2016, and 30% for a family plan.

- Despite significant increases in premiums since 2006 in the employer-sponsored market, the increases are modest compared to the increases in the late 1990s and early 2000s.

- The average deductible for individual and family employer-sponsored plans in Utah both nearly doubled from 2006-2016.

- On average, premiums for both individuals and families with employer-sponsored health insurance in Utah remain below a broadly accepted affordability benchmark of 10% of median income.

- The benchmark silver plan on the federal Marketplace in Salt Lake County increased 62% from 2017 to 2018, in part to compensate for the loss of federal cost-sharing reduction subsidies in the Marketplace.

- Half of Utah Medicare beneficiaries are low- to moderate-income, but do not qualify for Medicaid, potentially leaving them with high medical cost-burdens.

- In recent years, the key factors increasing insurance premiums nationally include: the rising cost of health care, increased risk in the health insurance pool, the loss of federal subsidies, uncertainty in national health care policy and consolidation in the insurance industry.

Download the full research report here: full report.

Download a summary of the report here: one-pager.

Download Part I of this series: Part I.