State lawmakers are currently considering a small personal and corporate income tax cut for Utahns that would reportedly reduce the state income tax from 5% to 4.95%. Lawmakers are considering these tax cuts in light of large revenue growth from the income tax on top of a one-time windfall as a result of the recent federal income tax overhaul. This brief addresses the impact of the personal income tax cut on households.

Based on data Utah Foundation has pulled together for a forthcoming report on Utah’s income tax, this tax reduction would have a fairly small impact on households. Among the upcoming report’s other findings:

- The highest-earning 20% of income tax filers produce two-thirds of income tax revenue. They also earn 60% of the income in the state.

- The bottom half of earners generate only 7% of Utah’s income tax revenue.

- Utah’s top marginal income tax rate of 5% ranks 30th nationally; however, Utah’s income tax burden of $27.51 per $1,000 of personal income ranks 16th nationally.

- Among Utah’s six neighboring states, only Idaho’s top tax rate is higher. Two neighboring states, Nevada and Wyoming, collect no income tax.

- Utah’s largest tax credit, the Taxpayer Tax Credit, reduces state revenue by about $1.2 billion in 2016.

- While the nominal 5% tax rate applies to all income earners, the Taxpayer Tax Credit reduces the median effective rate (the rate people actually end up paying) to 3%.

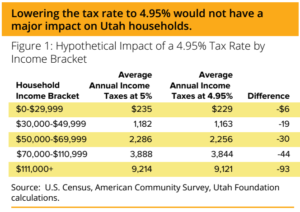

Figure 1 outlines how much Utah households paid in 2016 (the most recent year with comprehensive data available), and how much they would have paid if their tax rate was 4.95% instead of 5%. Media reports on the .05% tax cut place the impact between $20 million and $55 million. Utah Foundation’s estimates and the estimates from the Utah’s Office of the Legislative Fiscal Analyst’s tax rate simulator place the number around $40 million.

Figure 1 outlines how much Utah households paid in 2016 (the most recent year with comprehensive data available), and how much they would have paid if their tax rate was 4.95% instead of 5%. Media reports on the .05% tax cut place the impact between $20 million and $55 million. Utah Foundation’s estimates and the estimates from the Utah’s Office of the Legislative Fiscal Analyst’s tax rate simulator place the number around $40 million.

Utah Foundation estimates that in order to roll back the full impact of an $80 million tax windfall from the federal income tax changes, rates would need to be reduced to 4.90%. That would match Utah’s rate with New Mexico’s and roughly double the household impacts mentioned above. However, even at double the impact for households, it would not have a major effect on the taxpayer’s pocketbook.

Another way to look at the question is to consider how the money might be spent with no tax cut. The income tax is dedicated to education. An additional $80 million, if directed at the K-12 education system for instance, would represent another 2.8% increase in the weighted pupil unit (current legislation reportedly aims to increase the weighted pupil unit by 4%).

In its forthcoming report, Utah Foundation will delve into state income taxes more deeply.

Sources for this brief include 2018 HB 355, The U.S. Census Bureau, The Utah State Tax Commission, Utah’s Office of the Legislative Fiscal Analyst, The Tax Foundation, The Salt Lake Tribune, and Utah Policy. For more detailed endnotes see the forthcoming report.